By: Ananya Gokhale, Taylor Lien, Michael Loguercio, Alejandra Mantilla Diaz, Rui Wang

This study examines what drives loyalty among 18-34 age streaming consumers. The problem we looked to solve through our study is how Roku can better reach older Gen Z (18-24) and younger millennials (25-34) and retain them, beyond an initial one-time acquisition. This is especially relevant in an age where streamers are continually competing with each other and other media companies for the consumer's attention. Part I analyzes the conceptual groundwork for our research, tracing the evolution of the streaming market, reviewing prior literature on Gen Z and millennial viewing habits, and introducing our mixed-methods research approach. Part II of this research will present the empirical findings, industry interview insights, and final analysis and recommendations for Roku.

Why loyalty matters in a buyer’s market

In an age where the choices for entertainment are overwhelming, how does a streaming service keep customers returning? Moreover, how do platforms, such as Netflix, Hulu, or Tubi, turn consumers aged 18-34 into loyal users when they would rather scroll on TikTok than watch the latest season of TV? In the current TV landscape, streamers not only compete against each other for attention but also against the multitude of content that consumers can choose. Streaming platforms must continue to adapt to an evolving landscape. We analyzed the factors that kept our target demographic loyal, specifically through the lens of brand building, price sensitivity, and premium content. This investigation was conducted to assist Roku, a streaming technology company with an operating system that can be found on smart televisions and streaming devices.

Roku’s operating system allows consumers to easily access any streaming platform, search across platforms to find their favorite shows, and watch hundreds of live FAST channels (Roku, n.d.). By understanding what factors influence consumers’ loyalty aged 18-34 to specific platforms, Roku will be able to retain this demographic while also having invaluable information to advise streaming partners.

Importance of the Study

Brand Building

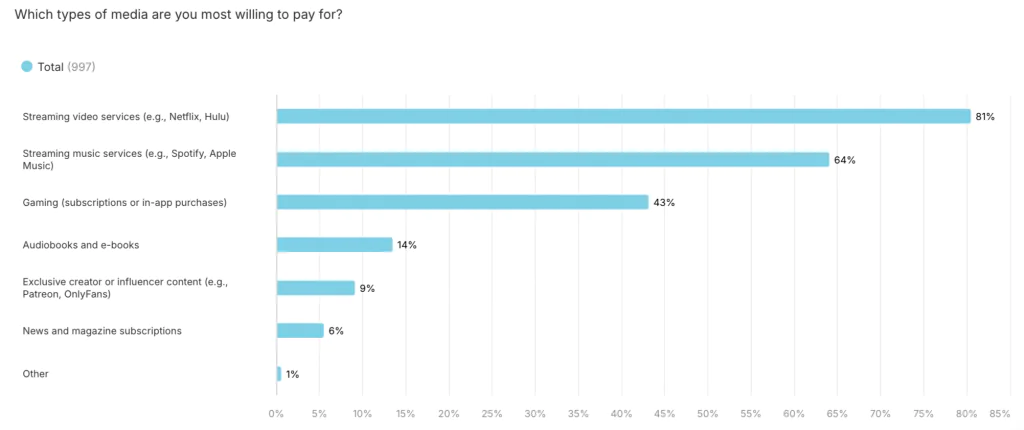

The marketplace of attention is a buyer’s market more than ever, and older Gen Z (18-24) and younger Millennials (25-34) are habitually interacting with multiple modes of entertainment on a given day. For example, 81% of Gen Z said that they spent 1 or more hours a day on social media, while simultaneously 72.9% spent over an hour on paid streaming services (Rand, 2024).

Figure 1: Gen Z Daily Media Consumption: Streaming Leads as the Only Platform They Consistently Pay For. Source: Ask Attest

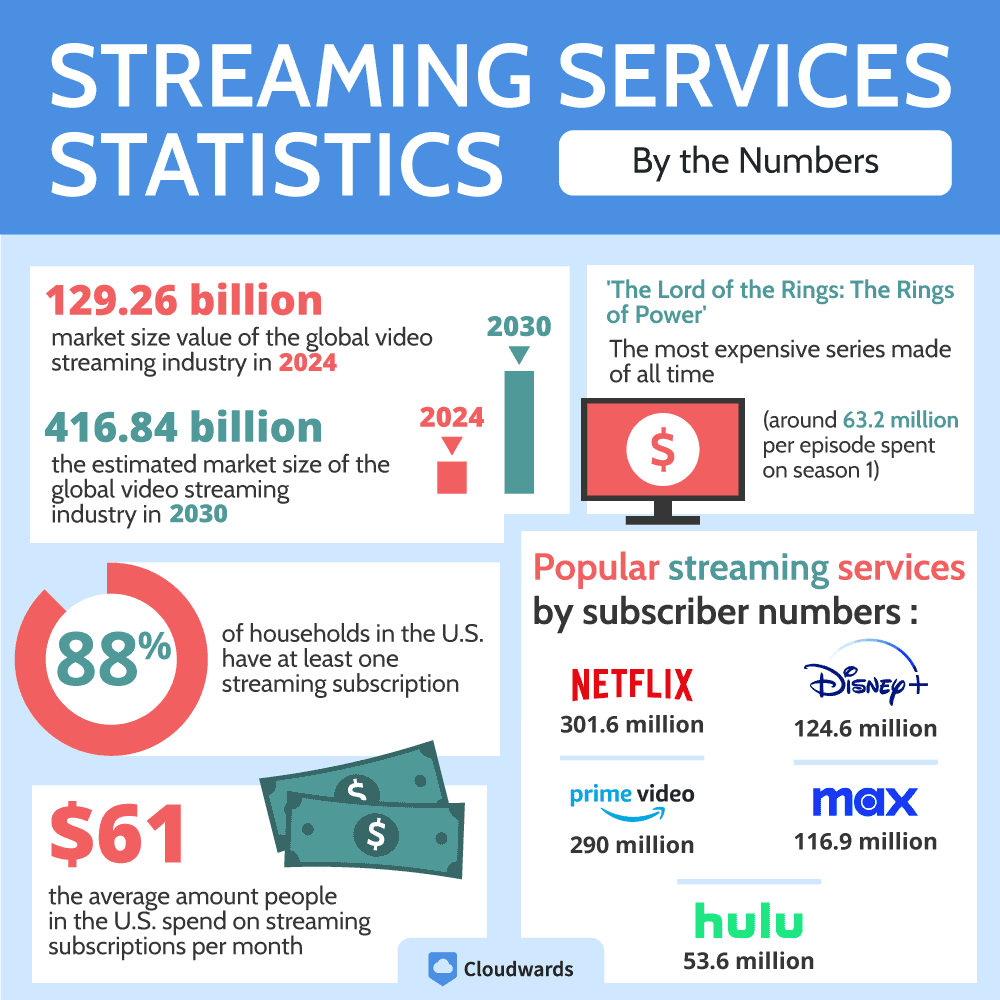

Figure 2: Streaming market infographic. Source: Cloudwards

In an age of constant disruption, the number of players vying for attention is likely to increase; therefore, establishing loyalty is paramount to a brand’s survival as the streaming market size is projected to reach $416.84 billion by 2030 (Pattison, 2024).

Price Sensitivity

As the number of streaming platforms has increased, these companies experimented with their own value proposition for consumers. Notably, in November 2022, Netflix added an ad- supported tier, which provided viewers with flexibility in how they pay for content (Rizzo, 2024). Additionally, streamers have collaborated with each other and various services to bundle their product with other subscriptions to provide consumers with deals. For example, a consumer can bundle Disney+, Hulu, and Max for $16.99 with ads, or, by subscribing to Walmart+, they can receive a Paramount+ subscription (Sheppard, 2025). Bundling provides an incentive to subscribe and save money, but it has not shown a significant effect on increasing loyalty, as it only boosted customers' decision to continue a subscription by 15% (Pattison, 2024).

Additionally, as streamers crack down on password sharing, young family members are removed from shared accounts and must decide which services they are willing to pay for with their limited purchasing power. Understanding how our target demographic approaches different subscription tiers and bundling deals can inform streaming platforms’ strategies to acquire and retain Gen Z and Millennial audiences.

What is Premium?

Historically, premium content referred to shows on cable channels such as HBO and Starz, that had high production value and which consumers had to pay extra to access ("basic vs. premium cable," n.d.). However, in the context of our study, premium content refers to any form of TV, whether that be scripted, non-scripted, or live event, that consumers would be willing to pay more to access. Furthermore, streaming services are not only TV providers but platforms providing consumers with a user experience. As a result, consumers are not only willing to pay more for content, but for a more efficient user experience. For example, when asked what consumers would pay more for, among the top answers were “large content library” and “simple interface” (Pattison, 2024). Unsurprisingly, Roku has more data on the streaming habits of older consumers (ages 35 and up) than consumers in the 18-34 age group. Our access to the older Gen Z and young Millennial demographic allows Roku to glean valuable insights about how to transform their strategy in the coming years to maximize growth and revenue. Therefore, understanding what this age group will pay for requires analyzing both how content and user experience affects what they see as premium.

Definition of Terms

The following definitions are critical to understanding our research, as these terms are used frequently throughout our paper and within the streaming and digital entertainment landscape at large.

AVOD: Ad-supported video on demand; offers on-demand libraries, either ad-supported or via hybrid plans ("Navigating the World of Streaming," 2024)

Bundling: Streaming companies combining multiple channels or content libraries into one subscription plan ("Television Studies Review," 2025)

Churn rate: Percentage of subscribers who cancel their subscriptions over a given period

FAST: Free ad-supported streaming television; provides free linear viewing supported by ads (Navigating the World of Streaming, 2024)

Linear TV: Traditional broadcast television model delivered through cable, satellite, or "over the air" (Vinikas, 2024)

Premium content: Highly curated, digital video content curated to target a specific audience ("Premium Video," 2022)

SVOD: Subscription video on demand; gives subscribers premium ad-free content (Navigating the World of Streaming, 2024)

Review of Literature

Trends in Gen Z and Millennials

The research available that studies streaming trends across age groups highlights that consumers aged 18-34 are adept at cancelling and managing their streaming budgets. In a 2024 Deloitte study, 53% of Gen Z and Millennials canceled at least one streaming service in the previous 12-month period (Westcott et al., 2024). Similarly, in 2023, 39% of Gen Z and 46% of Millennials cut a streamer in the last six months to reduce costs compared to 35% and 28% of Gen X and Boomers, respectively (Purdy & Willis, 2023). These datasets emphasize the younger generations' propensity to churn compared to their older counterparts, reinforcing the challenge of creating perennial subscribers.

Churn and Loyalty

Although loyalty is intangible, studies indicate that Amazon Prime has the lowest churn rate at 8% (Butts, 2024). As Prime provides value beyond access to their streaming catalog, giving consumers free shipping in online retail, thus, consumers may be less likely to cancel the service. Netflix has a marked advantage by being the first mainstream streaming service and, as a result, has the second-lowest churn rate at 9% (Butts, 2024). This corroborates a recent study that found that subscribers of 4+ years are five times less likely to cancel (Adgate, 2024). The study highlights that if using a specific platform becomes a long-term habit for consumers, it greatly minimizes the chance of churn.

Price Flexibility

Various studies show that consumers are cognizant of price when making cancellation decisions. When asked why they unsubscribed (39%), the top reason for cancelling was to save money (Vorhaus Advisors, 2024). This is consistent with a KPMG study where 38% of participants stated they cancelled a subscription due to price increases (Purdy & Willis, 2023). The prevalence of price as a factor for cancellation illustrates that consumers are alert and sensitive to pricing changes and make active decisions about their streaming behavior based on cost.

Current State of the Industry

The industry's most crucial issue is how to best monetize TV alongside new technology. Consumers have now adapted to the fact that most television content is available on streaming platforms paid for with a monthly or annual subscription. The relationship between where a show was produced and where it can be watched has been altered. For example, many HBO legacy titles are now available to stream on Netflix after being available exclusively on Max for most of the platform’s existence. This may bring new audiences into HBO content, but it may erode the long-standing relationship HBO has with its audience.

From a consumer perspective, it makes the choice of why you should subscribe to one service over the other much more elusive. For example, Netflix is not a destination for any one type of content, it’s a platform that has something for everybody, a modern equivalent of channel surfing.

In linear television, consumers knew where to watch something, when to watch it, and what each channel was generally offering. Those habits have changed with the introduction of streaming services, consumers can watch whatever they want whenever they want, making visibility a greater challenge.

An Overview of the World

With the continuous emergence of new streaming platforms, services being bundled and unbundled, and companies merging and acquiring others, there is a lack of consistency that once existed before streaming became prevalent. Additionally, consumers can stream from anywhere at any time with an overwhelming amount of content being available to them. Viewers are navigating between platforms to follow their favorite content. They subscribe only to unsubscribe, enjoying a quick binge-watching session, as new content becomes available in various places. The goal of our study is to research what factors might compel the 18-34-year-old audience to remain loyal and how individual streamers can stand out in a crowded marketplace.

Summary

With younger generations not having grown up with the same consumer expectations as previous generations, new challenges arise in engaging younger consumers. There are more options than ever regarding how and when to spend someone’s time and attention. Chapter three will discuss our survey findings, as well as the expert interviews with industry leaders.

-

Adgate, Brad. 2024. “Reducing SVOD Churn Should Be the Next Priority with Media Companies.” Forbes, April 1, 2024. https://www.parksassociates.com/blogs/in-the-news/parks-prime-video-has-lowest-churn-rate.

Apple TV+: Potential for Growth. 2023. Parrot Analytics, November 7, 2023. https://www.parrotanalytics.com/insights/apple-tv-potential-for-growth/.

“Basic vs. Premium Cable.” n.d. Fiveable. Accessed April 6, 2025. https://library.fiveable.me/key-terms/television-studies/basic-vs-premium-cable.

Blake, Sarah. 2024. “The State of Digital Content Piracy in 2024.” CordCutting.com, April 23, 2024. https://cordcutting.com/research/content-piracy-study/.

Auxier, Brooke, and Lee Rainie. 2019. “Americans Concerned, Feel Lack of Control over Personal Data Collected by Both Companies and the Government.” Pew Research Center, November 15, 2019. https://www.pewresearch.org/internet/2019/11/15/americans-concerned-feel-lack-of-control-over-personal-data-collected-by-both-companies-and-the-government/.

“Bundling.” n.d. Fiveable. Accessed April 6, 2025. https://library.fiveable.me/key-terms/television-studies/bundling.

Butts, Tim. 2024. “Parks: Prime Video Has Lowest Churn Rate.” TV Technology, May 30, 2024. https://www.tvtechnology.com/news/parks-prime-video-has-lowest-churn-rate.

Byrne, Claire. n.d. “How Quizzes Boost Your Content: The BuzzFeed Quiz Phenomenon.” Involve.me. Accessed April 6, 2025. https://www.involve.me/blog/how-quizzes-boost-your-content-the-buzzfeed-quiz-phenomenon.

CacheFly. 2024. “Exploring the Opportunities and Challenges of Niche Streaming Services.” July 3, 2024. https://www.cachefly.com/news/exploring-the-opportunities-and-challenges-of-niche-streaming-services/.

Deloitte. 2024. “Social Media and Creators Drive Viewers to TV Shows, Movies, and Games.” Deloitte Insights, November 13, 2024. https://www2.deloitte.com/us/en/insights/industry/technology/digital-media-trends-consumption-habits-survey/2024/online-creators-and-the-impact-of-social-media-on-entertainment.html.

Deloitte. 2025. “2025 Digital Media Trends: Social Platforms Are Becoming a Dominant Force in Media and Entertainment.” Deloitte Insights, March 25, 2025. https://www2.deloitte.com/us/en/insights/industry/technology/digital-media-trends-consumption-habits-survey/2025.html.

Eco Consultancy. 2022. “HBO Max Boosts US Engagement and Viewing with Interactive Fantastic Beasts Campaign.” Accessed April 6, 2025. https://econsultancy.com/case-studies/view/hbomax-boosts-engagement/.

Forrest Brown. n.d. “Criterion Channel Part 1.” Accessed April 6, 2025. https://www.forrestsbrown.com/criterion-channel-part-1.

Grothaus, Michael. 2023. “Older Millennials Prefer Streaming TV, while Gen Z Opts for User-Generated Content.” Fast Company, July 27, 2023. https://www.fastcompany.com/90929341/older-millennials-vs-gen-z-streaming-tv-likes.

Index Exchange. 2024. “Improving Content Discovery in Streaming TV: Plex.” May 22, 2024. https://www.indexexchange.com/2024/05/22/improving-content-discovery-streaming-tv-plex/.

Kadence. 2025. “Top 4 Trends Set to Disrupt the Media Industry in 2025.” Accessed April 6, 2025. https://kadence.com/top-4-trends-set-to-disrupt-the-media-industry-in-2025-2/.

Kelly, Colin. 2024. “Tubi Refreshes Brand to Build on Momentum with Young, Diverse Audiences.” Marketing Dive, February 29, 2024. https://www.marketingdive.com/news/tubi-brand-refresh-avod-streaming-wars/708882.

Meaney, John. 2025. The Impact of Live Event Programming on Streaming Platform Growth. Media Insights Press.

Meaney, Matt. 2025. “Netflix Is Signing Up More People to Watch Its Live Sports, but That’s Only Half the Battle.” Business Insider, February 27, 2025. https://www.businessinsider.com/netflix-live-sports-streams-acquire-millions-subscribers-charts-2025-2.

Murray, Conor. 2023. “Spotify Wrapped 2023 Comes Soon: Here’s How It Became a Viral and Widely Copied Marketing Tactic.” Forbes, November 28, 2023. https://www.forbes.com/sites/conormurray/2023/11/28/spotify-wrapped-2023-comes-soon-heres-how-it-became-a-viral-and-widely-copied-marketing-tactic/.

“Navigating the World of Streaming: Understanding FAST, AVOD, SVOD and TVOD.” n.d. NewscastStudio. Accessed April 6, 2025. https://www.newscaststudio.com/2024/02/29/navigating-the-world-of-streaming-understanding-fast-avod-svod-and-tvod/.

Netflix vs. Everyone with Content Chief Bela Bajaria, Part 1. 2025. Puck, podcast audio, February 13, 2025. https://podcasts.apple.com/us/podcast/netflix-vs-everyone-with-content-chief-bela-bajaria-part-1/id1612131897?i=1000692087173.

Newman, Jared. 2024. “The Brilliant Roku Feature That Time Forgot.” TechHive, January 5, 2024. https://www.techhive.com/article/2192717/the-brilliant-roku-feature-that-time-forgot.html.

Nielsen. 2023. “Data-Driven Personalization: The Future of Streaming Content Discovery.” Nielsen, August 8, 2023. https://www.nielsen.com/insights/2023/data-driven-personalization-2023-state-of-play-report/.

Parrot Analytics. 2023. “Growing Demand for Adult Animation.” December 6, 2023. https://www.parrotanalytics.com/insights/growing-demand-for-adult-animation/.

Parrot Analytics. 2023. “Why Young Adult Programming Is Key to the Future of Streaming Platforms in the US.” February 28, 2023. https://www.parrotanalytics.com/insights/why-young-adult-programming-is-key-to-the-future-of-streaming-platforms-in-the-us/.

Parrot Analytics. 2024. “What Are the Most Loved Movie Genres for Each Generation?” October 6, 2024. https://www.parrotanalytics.com/insights/movie-genre-preferences-each-generation-millennials-genz-genx/.

Parrot Analytics. n.d. “Streamer Strategies for Audience Retention without Prestige Linear Series.” Parrot Analytics Academy. Accessed April 6, 2025. https://www.parrotanalytics.com/academy/streamer-strategies-for-audience-retention-without-prestige-linear-series.

Pattison, Sandra. 2024. “35 Streaming Services Statistics You Need to Know in 2025.” Cloudwards, July 7, 2024. https://www.cloudwards.net/streaming-services-statistics/.

Pew Research Center. 2017. “About 6 in 10 Young Adults in U.S. Primarily Use Online Streaming to Watch TV.” September 13, 2017. https://www.pewresearch.org/short-reads/2017/09/13/about-6-in-10-young-adults-in-u-s-primarily-use-online-streaming-to-watch-tv/.

Pot, Justin. 2017. “How to Use Roku Feed to Keep Up with New Episodes of Your Shows.” How-To Geek, April 14, 2017. https://www.howtogeek.com/300362/how-to-use-roku-feed-to-keep-up-with-new-episodes-of-your-shows/.

Purdy, Suzanne, and Emily Wills. 2023. “Consumers Loyal to Streaming, but at What Price?” KPMG Media Consumer Survey. https://kpmg.com/us/en/articles/2023/consumers-loyal-to-streaming-what-price.html.

Rand, Stephanie. 2024. “Gen Z Media Consumption 2025: Social Media & What’s Next.” Attest, November 15, 2024. https://www.askattest.com/blog/research/gen-z-media-consumption.

Rizzo, Lillian. 2024. “Netflix Ad-Supported Tier Has 70 Million Monthly Users Two Years after Launch.” CNBC, November 12, 2024. https://www.cnbc.com/2024/11/12/netflix-ad-supported-tier-70-million-monthly-users.html.

Roku. n.d. “What Is Roku – How the Roku Experience Works.” Accessed May 1, 2025. https://www.roku.com/what-is-roku.

Singer, Michael. 2024. “Personalizing Growth.” Deloitte Digital, June 11, 2024. https://www.deloittedigital.com/us/en/insights/research/personalizing-growth.html.

“TV & Streaming Video Advertising Glossary.” 2022. AudienceXpress, June 9, 2022. https://audiencexpress.com/insights/blog/premium-video-advertising-glossary/.

Vinikas, Ieva. n.d. “Linear TV: All You Need to Know.” Kaltura. Accessed April 6, 2025. https://corp.kaltura.com/blog/linear-tv-all-you-need-to-know/.

Vorhaus Advisors. 2024. “Canceling Streaming Subscription: Reasons U.S. 2024.” Statista, May 2024. https://www-statista-com.cmu.idm.oclc.org/statistics/1290078/reasons-video-service-subscriptions-cancellation/.

Westcott, Kevin, Chris Arkenberg, Jana Arbanas, and Jeff Loucks. 2024. “Streaming Video at a Crossroads: Redesign Yesterday’s Models or Reinvent for Tomorrow?” Deloitte Insights, March 20, 2024. https://www2.deloitte.com/us/en/insights/industry/technology/digital-media-trends-consumption-habits-survey/2024/customization-and-personalization-lead-the-svod-revolution.html.

Widener, Chris, Jana Arbanas, Doug Van Dyke, Chris Arkenberg, Brandon Matheson, and Brooke Auxier. 2025. “2025 Digital Media Trends: Social Platforms Are Becoming a Dominant Force in Media and Entertainment.” Deloitte Insights, March 25, 2025. https://www2.deloitte.com/us/en/insights/industry/technology/digital-media-trends-consumption-habits-survey/2025.html.

Winslow, George. 2024. “If Bundling Is Back, What’s the Ideal Bundle?” TV Technology, May 17, 2024. https://www.tvtechnology.com/news/if-bundling-is-back-whats-the-ideal-bundle.