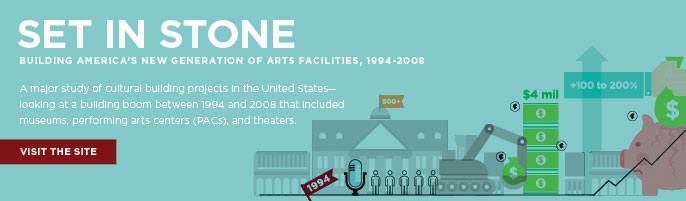

Recently, the University of Chicago’s Cultural Policy Center released the report, “Set in Stone: Building America’s New Generation of Arts Facilities, 1994-2008.”

Summary: The research examines the boom of major cultural building projects (museum, performing arts centers, and theaters) between 1998 and 2004, specifically looking at the decade between 1990 and 2000. The findings indicate during that period, “the level of investment in bricks and mortar as a percentage of total revenue and assets was disproportionate.” The full report addresses the landscape of cultural building, the investment determinants of cultural building, the feasibility of cultural building projects, and the effects on communities. The report takes into account population change, the national trend in ratio of arts organizations to cultural facilities, the relationship between the number of existing facilities in an MSA and the population, GDP, economic climate, municipal spending on physical infrastructure, spending by type of project, education rates, median household income levels, distribution of costs of projects (by region), geographic considerations, and other factors affecting the supply, demand and sustainability of cultural building projects.

[embed]http://youtu.be/KwhG7SK9csc[/embed]

Case Studies: Four case studies, presented as teaching resources, portray complex, management situations students and professionals might encounter in the real world. The cases (comprised using internal documents , construction data, and first-hand accounts from administrators, board members and/or volunteers involved in each situation) emphasize the need for managers to make strategic decisions, weighing the benefits and risks of each potential course of action. These studies provide a platform for discussion about the strategic design of projects, potentially shaping future design and management practice.

The four case studies highlight issues of strategic decision making, project design, expansion and management at:

1) the Art Institute of Chicago in Chicago, IL

2) the AT&T Performing Arts Center in Dallas, TX

3) the Long Center for the Performing Arts in Austin, TX

4) the Taubman Museum of Art in Roanoke, VA

Key Findings: The report and the findings show that (taken from the report)

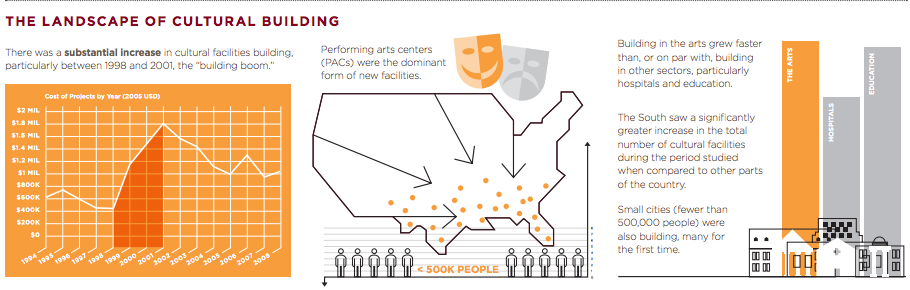

- Cultural institutions and arts facilities were overbuilt during the boom years

- Performing Arts Centers were the dominant form of new facilities

- The building boom affected the entire country, but was concentrated in the South, which saw enormous increases in the total number of facilities

- Building in the arts grew faster between 1998 and 2001 than or on par with building in other sectors, particularly health and education

- Rising population and higher average levels of education and income help explain why some cities built more than others

- There is no clear pattern of spillover effects (negative or positive) of specific cultural building projects on non-building local cultural organizations and the greater community

- There was far less investment in traditional theater facilities than there was in museum and performing arts centers

- The New York-Northern New Jersey-Long Island MSA spent more on cultural infrastructure ($1.6 billion) building than any other MSA during this period

- Research shows that for every additional cultural facility a city had, it invested between $0.11 and $0.23 more per capita per year in cultural building projects

- What influenced how much a city invested in cultural infrastructure was not the size of a city’s population, but how fast the population was increasing or decreasing

[embed]http://youtu.be/76vN7mb9n6E[/embed]

Looking Ahead: Joana Woronkowicz, co-author of the report, summarizes the lessons learned from the study and how the arts industry should proceed in making building project decisions.

• What is the motivation for the project?

• Does it align with organization’s artistic mission?

• Is there a need for the project (not a want), but a need?

• Do I have the leadership in place to take the project from the beginning to the end?

• Does the building project respond to the needs of the community?

• How can I be flexible in controlling expenses and nimble in generating income?